Many lenders help us pay for life’s needs and wants. They’ve built a wide mix of ways to borrow cash for almost anything. You can apply for the best quick loan to save the day. These can put cash in your hand within hours, not days. Online forms and fast checks make this speed trick work well.

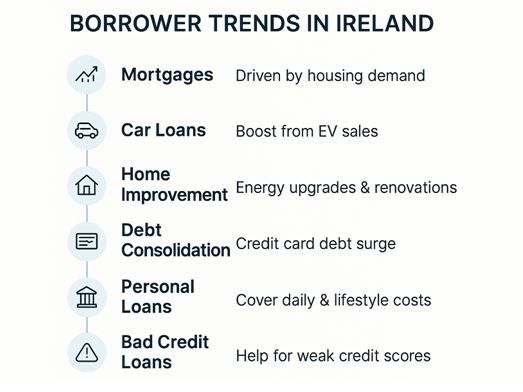

Many loan firms push the loan types that make them the most money. They look at both how much they earn and what people ask for. Some loan types rise above others in the busy money world. These stand out based on how much cash flows through them each day.

| Loan Products Popularity in Ireland | ||

| Loan Type | Popularity with Lenders | Main Reason |

| Personal Loans | High | Broad use, steady demand |

| Loans for Bad Credit | Medium | Risky but profitable |

| Mortgage Loans | Very High | Secured, long-term |

| Car Loans | High | Growth in auto sales |

| Home Improvement Loans | Medium-High | Linked to property value |

| Debt Consolidation | Medium | Rising card debt in Ireland |

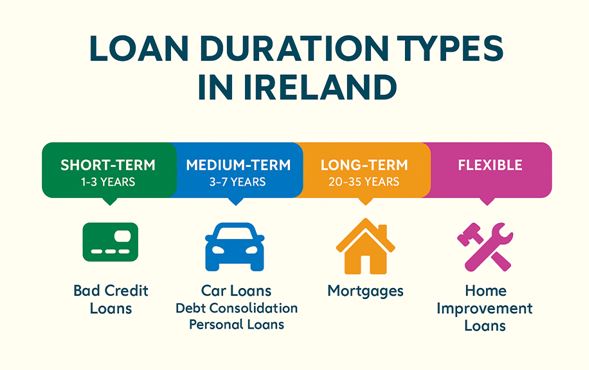

Home Improvement Loans

Individuals are shifting to home improvement loans to fix up their spaces. They’re using the money for broken bits, adding new rooms, or giving their kitchen a new look. The house itself stands as backup if someone can’t pay. This means less worry for the lender and often better rates for homeowners.

People are visiting preferred places instead of making improvements to their current homes. The pandemic pushed this even more as we all spend extra time at home.

Most loans range from €5,000 to €50,000, depending on the work needed. Some works, like adding a new floor, might need more, while smaller fixes cost less. The interest rates vary but tend to be more minor than those on credit cards.

You just require to deliver proof of income, good credit, and details about your home. Your approval can happen quickly, often within days for smaller amounts.

Debt Consolidation Loans

You can consolidate all your bills into one payment. The debt consolidation loans have become so popular lately. Many people can now apply for these debt consolidation loans online.

They like to have just one due date to track each month. Many people are getting these loans because of the rising debt problems in Ireland. These loans come with clear end dates, unlike endless credit card debt. Most run for three to five years with no surprises along the way. The fixed rate means your payment stays the same until you’re done.

Banks report fewer people dropping out of these plans than from other loans. Once someone starts paying, they tend to stick with it until the end. This makes these loans a safe bet for lenders.

You might get a loan amount from €5,000 to €25,000 based on what you owe. The best rates go to those with good credit scores and steady jobs.

Personal Loans

Personal loans offer quick funds for almost any use you can think of. Some people use them for surprise bills, while others buy new cars. You can spend this loan on anything. Many prefer this as they give freedom to many people, unlike home or car loans.

Most lenders now approve these loans within hours, not days. This draws in people who can’t wait for slower loan types. Their online forms take just minutes to fill out from your phone. The lenders know exactly how much will come in each month. The time span is fixed too, often between one and seven years.

You will have high approval rates when you have better credit scores. Most loans range from €1,000 to €25,000. There is no need to put up your house or car. These loans work purely on your promise to pay back. That said, failing to pay can still hurt your credit score.

Loans for Bad Credit

Some people hit rough patches that hurt their credit scores. These special loans give them a way forward when others say no. They work as a bridge back to better money and health.

Lenders know these loans come with more chances of missed payments. These loans have grown more common since the big money crash. Many people found their scores dropped after a job loss or illness.

The amounts tend to stay small, often between €500 and €5,000. This helps keep risks down for both sides of the deal. Smart lenders check income and job status very closely. Some lenders ask for a friend or family member to back the loan. Others might want something of value to hold just in case.

Car Loans

Car loans help people get cars they can’t pay for up front. These plans work for both new models and pre-loved vehicles. Most buyers spread costs over three to seven years of monthly bills.

More people want their own wheels but lack the cash pile needed. This gap has made car loans one of the busiest loan types. The lender can take the car back if someone stops paying. This safety net keeps rates lower than many other loans.

Most car buyers stick with their plans until the final payment. This means lenders can count on that money coming in. The best deals go to those with solid credit and good jobs. First-time buyers might need someone to sign with them.

Conclusion

The loan world keeps changing as both sides seek better deals. What works best now may shift as our money habits change. Many lenders watch these trends and adapt their offers quickly. The most popular ones solve common problems in simple and clear ways. The best loan companies have caught this wave and are riding it well.